Bill Would Freeze Fraudulent Lenders

Caveat emptor has always been an integral concept in free- market economies. It’s a Latin phrase encompassing the understanding that consumers are sophisticated adults capable of successfully engaging in commerce. But the concept of buyer beware is predicated on truth and transparency amid the transaction and is rendered impotent when fraud or misrepresentation strips buyers of their ability to utilize their skills and savvy as consumers. Unfortunately, fraud has played a significant role in the mortgage problems our nation now faces.

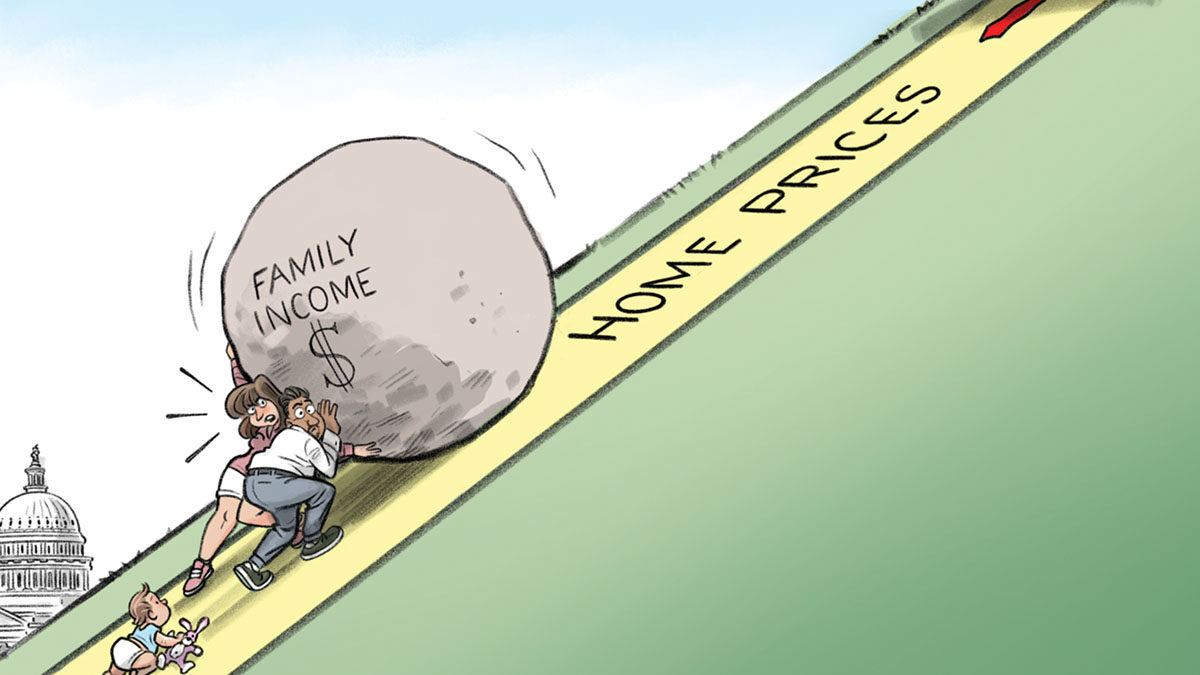

By now, we all know the magnitude of the mortgage crisis nationally, but no state has been as impacted as my own home state of Ohio, which recently had the dubious distinction of being ranked No. 1 in the nation in its percentage of houses in foreclosure. Ohio’s foreclosure rates have increased 138 percent since August 2006, and the number of foreclosure filings has nearly quintupled since 1995. Ohio’s foreclosure rate is as much a symptom of the state’s anemic economic health as it is a cause of it.

But statistics and rankings cannot begin to convey the impact of the mortgage crisis on a human level; there is no means of quantifying the fear, anxiety and devastation that results when a family loses its claim on home ownership. From a humanitarian or economic standpoint, America’s housing predicament cannot be tolerated.

The causes of the spike in foreclosure rates have been well-documented. Most who file for foreclosure still do so amid job loss, major illness or divorce. For these Americans, the federal government must aggressively offer financial and credit counseling and intervene early to help them avoid losing their homes. But a significant number of foreclosures stem from people who were victims of an overly aggressive subprime industry, or in many cases, predatory lenders.

For many Americans, the terms subprime and predatory have become synonymous. This is an unfortunate and misconceived perception. Lending has always been built upon risk, and the subprime industry has effectively placed millions of American families into homes whose credit was deemed too risky for conventional loans. Subprime lending expanded dramatically during the past decade. The public was sold the concept of home ownership as the cornerstone of the American dream. Ownership rates rose to their highest levels in history, and the housing boom appeared endless. Subprime lenders helped to fuel this fire with interest-only loans, piggyback loans, adjustable rate mortgages with initial teaser rates, and “no-documents” and “NINJA” loans (no income, no job, no assets), to get more and more Americans into homes. But at some point, we all knew the piper would need to be paid.

Buyers cannot beware when fraudulent lenders misinform the borrower or manipulate them through aggressive sales tactics. Predatory lending is not solely responsible for the myriad problems facing the mortgage industry and housing market, but it has contributed mightily to the plight. The FBI reports that mortgage fraud has risen 237 percent in the past five years, and according to the Treasury Department, mortgage fraud has increased more than 1,400 percent since 1997. Predatory lending is, by definition, pernicious, and we must enhance regulators’ and law enforcement’s abilities to prevent it and increase the punishment for those who engage in it.

Predatory lenders must be given no quarter, but it is important that in our efforts to crack down on them, we do not exacerbate the housing slump by restraining liquidity for future loans. Significant overhaul and regulation of the subprime industry will have a broad effect on the housing market and could dry up credit to Americans who desperately need it.

Recognizing the dexterity needed in crafting legislation that will not adversely impact the housing market, last month House Financial Services ranking member Spencer Bachus (R-Ala.), the late Rep. Paul Gillmor (R-Ohio) and I introduced the Fair Mortgage Practices Act, a bill to protect homebuyers from unscrupulous lenders or fraudulent lending tactics while preserving the benefits that subprime lending has brought to low- and middle-income Americans.

The bill targets the unsavory and predatory practices that have accelerated the problems in the mortgage industry. Most importantly, the bill authorizes $20 million for the Department of Justice to prevent, investigate and prosecute mortgage fraud. It creates a national licensing process to increase professionalism and adherence to ethics among brokers. The bill also establishes a new federal standard to prevent appraiser intimidation and protect an appraiser’s independence, helping ensure that a home’s value is properly estimated. It enhances the federal oversight of state appraisal programs, improves appraiser licensing and educational standards, and prohibits “appraisal pressure” and coercion, extortion and bribery by lenders, realtors, brokers and sellers of appraisers.

The comprehensive Fair Mortgage Practices Act protects consumers by better policing the mortgage industry and ensuring that borrowers are armed with simplified and transparent information to make educated and financially beneficial decisions. The bill restricts prepayment hybrid ARM penalties and requires subprime borrowers to have escrow accounts for taxes and insurance established at the time of consummation of the loan. The answer to America’s mortgage industry woes is consumer education, clear disclosure and better regulation of mortgage brokers; our legislation will keep our housing markets strong while helping ensure that the interests of homebuyers are being protected both at the point of sale and in the future.

Moreover, the market already is correcting itself. Lenders are tightening credit, requiring larger down payments and ending some of their more creative and complicated financing mechanisms. In a sense, the industry is reverting to the some of the same — more conservative lending requirements it adhered to prior to the housing boom — a trend that should be welcomed by lawmakers.

As the drums continue to beat for Congress to remedy the mortgage crisis, we all would be wise to take heed of another Latin phrase, one reminding Congress of the dangers of wielding an overly aggressive regulatory hand: Primum non nocere (first, do no harm).

Rep. Deborah Pryce (R-Ohio) is ranking member of the Financial Services Subcommittee on Capital Markets, Insurance and Government-Sponsored Enterprises.