Tax Cut for Booze Could Lead to More Drinking Deaths

Researcher estimates increase in disease, accidents as result of reduction in taxes

Tax cuts for alcohol producers in the Senate’s tax code overhaul could result in around 1,500 more alcohol-related deaths each year, according to a researcher at the Urban-Brookings Tax Policy Center.

The tax bill, which the Senate could vote on later this week, would provide a $4.2 billion tax break over two years for the makers of beer, wine and spirits. While lawmakers have framed the change as a benefit for smaller producers of craft beverages, large global conglomerates that dominate the industry would likely get the bulk of the savings.

“The industry now supports about 15,000 jobs. Sixty-one new breweries have opened just last year alone in Ohio,” Sen. Rob Portman said at the Finance Committee’s markup of the tax proposal earlier this month. “This legislation is only going to promote the expansion and the jobs that come with these entrepreneurial small businesses.”

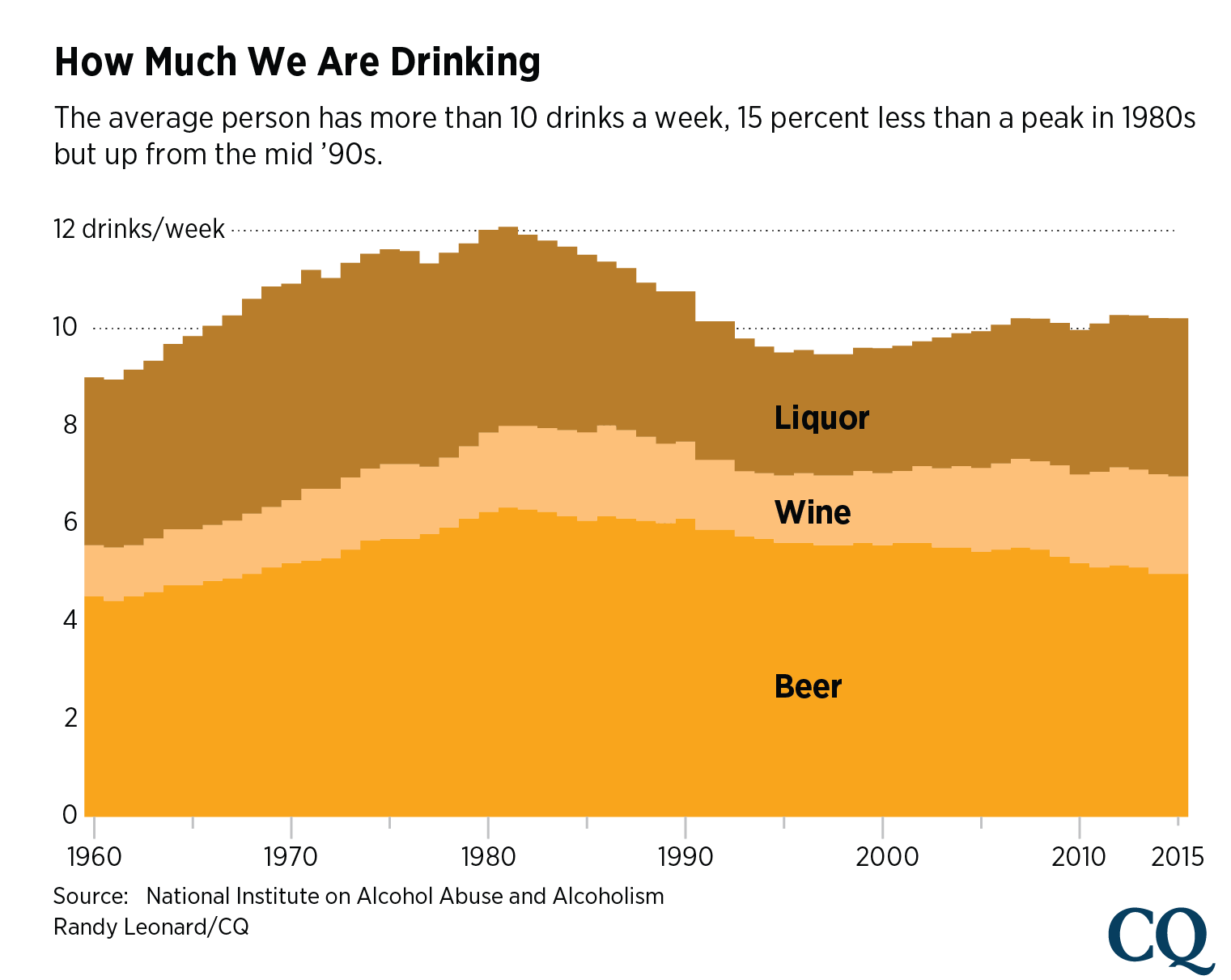

Health researchers who study the role that taxes play in reducing alcohol consumption say that a tax cut could lead to more drinking. That could result in more illnesses and deaths associated with excessive alcohol use.

Adam Looney, a senior fellow for economic studies at the liberal-leaning Urban-Brookings, crunched the numbers and estimated that the industrywide 16 percent tax cut would result in between 281 and 659 traffic-related deaths per year, and about 1,550 total deaths from all alcohol-related causes. Those estimates were based on previous studies that found increases in the tax to have the reverse effect on crashes and health outcomes.

In addition to the potential for increased alcohol consumption, Looney argued that the bill’s changes to how imported alcohol products are taxed would be difficult to enforce. The current alcohol excise tax is designed so that smaller businesses pay a lower rate up to a certain amount produced. Looney argues that the preferential rates for smaller manufacturers already make the tax difficult to administer, since it requires tax collectors to verify how much is being produced.

The bill would apply some of those rates to both larger companies in the United States and producers overseas.

Looney, a tax policy official at the Treasury Department during the Obama administration, said it could be easy to exploit the proposed policy.

“For instance, a large French producer who would not otherwise qualify for the lower rates could divide its production among multiple labels or multiple importers, each below the 250,000 bottle limit, evading the tax and producing a comparative advantage for the foreign producer over the American producer,” Looney wrote. “Even for a foreign producer with greater than 250,000 bottles of production, it would be unclear which 250,000 bottles (or 100,000 gallons of spirits, or 60,000 barrels of beer) would qualify for the reduced rate, allowing multiple importers or distributors to claim (or attempt to claim) the tax benefit.”

Looney suggested that lawmakers ought to reverse course and raise taxes on alcohol, arguing that current rates don’t come close to paying for the external costs related to alcohol use.

“Rather than establishing new tax preferences based on production levels and volumes — which are hard to enforce, complicated, and economically unjustified — a better approach is to harmonize the tax rate across beverages based on alcohol content and eliminate the special preferences and credits that currently exist based on production volume or use of flavors or additives,” he wrote.

Correction | Nov. 28, 2017, 3 p.m. | An earlier version of this story misstated an estimate contained in an Urban-Brookings Tax Policy Center report. Around 1,500 additional alcohol-related deaths per year will result from the proposed alcohol tax cut, according to the report.