Retirement savings bill seeks small business buy-in

Bipartisan momentum for change comes as retirement crisis looms

The House on Thursday will take up what could be the most significant changes in retirement savings policy in more than a decade.

But the bill’s backers acknowledge it’s just an initial step in addressing what critics call a huge hole in Americans’ nest eggs, at a time when traditional pension plans are increasingly rare and Social Security is facing financial headwinds.

The bill headed to the House floor would, among other things, create incentives for businesses to provide access to workplace savings plans for some of the most underserved groups — employees at small businesses and part-time workers.

“Employer-sponsored retirement plans and IRAs are valuable tools successfully used by millions of Americans to help save for retirement,” says the Ways and Means Committee report accompanying the bill, approved by voice vote April 2. “The Committee believes that it should be easier for Americans to use these accounts to save. The Committee also believes that it should be easier for employers to offer retirement plans to their employees.”

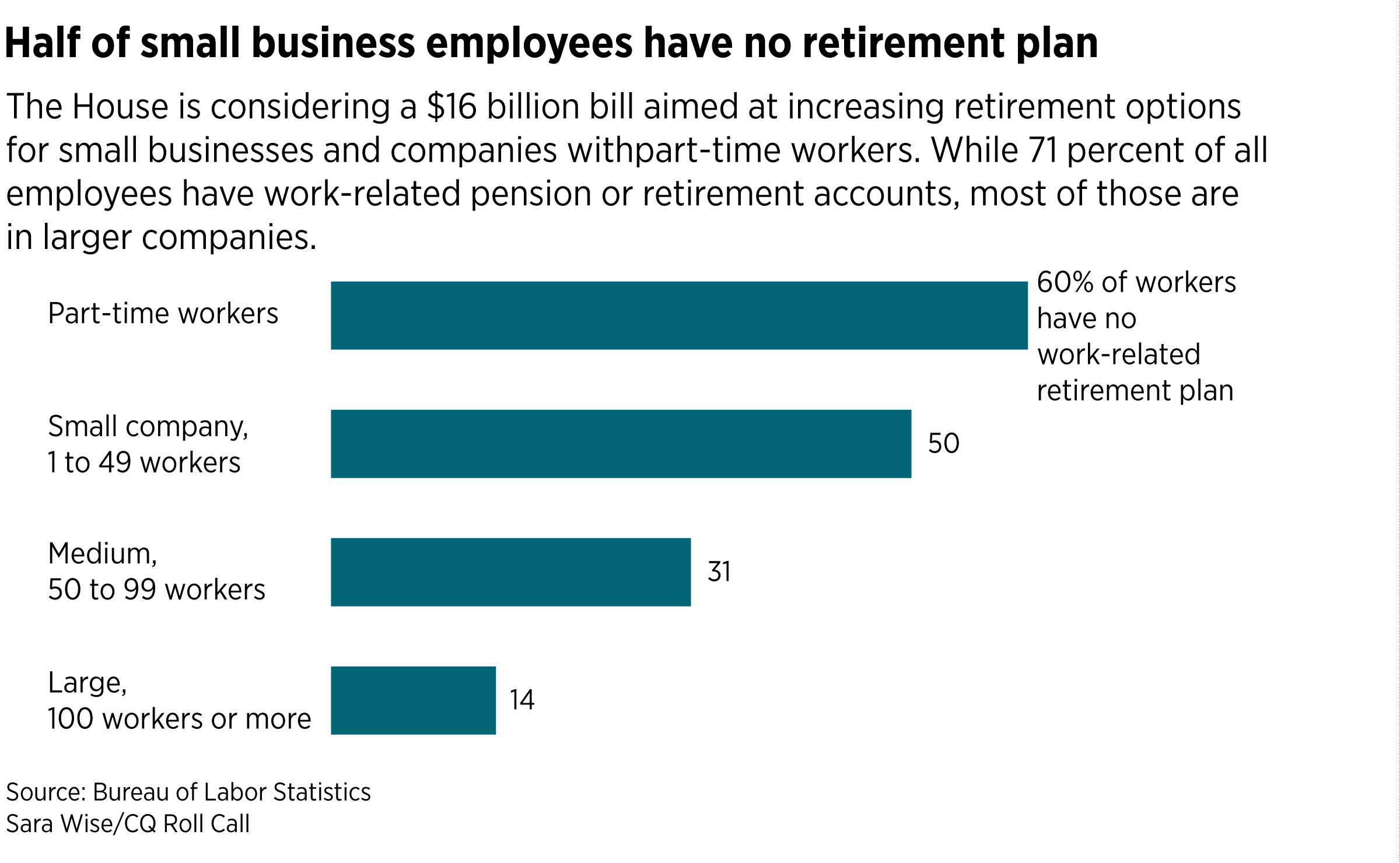

Overall, 71 percent of the civilian workforce has access to workplace retirement savings plans, but only 55 percent participate, according to Bureau of Labor Statistics figures. The numbers are much worse for groups targeted by the bill: Just 36 percent of employees at companies with fewer than 50 workers are enrolled, and just 23 percent of part-timers.

Some estimates put the number of Americans without access to employer-sponsored retirement accounts at 55 million or more. House Ways and Means Chairman Richard E. Neal often points out that 10,000 people a day start claiming Social Security, where the average yearly benefit is around $16,000.

Such numbers translate into a lot of Americans retiring into poverty, and lawmakers on both sides of the aisle are pushing legislation this year.

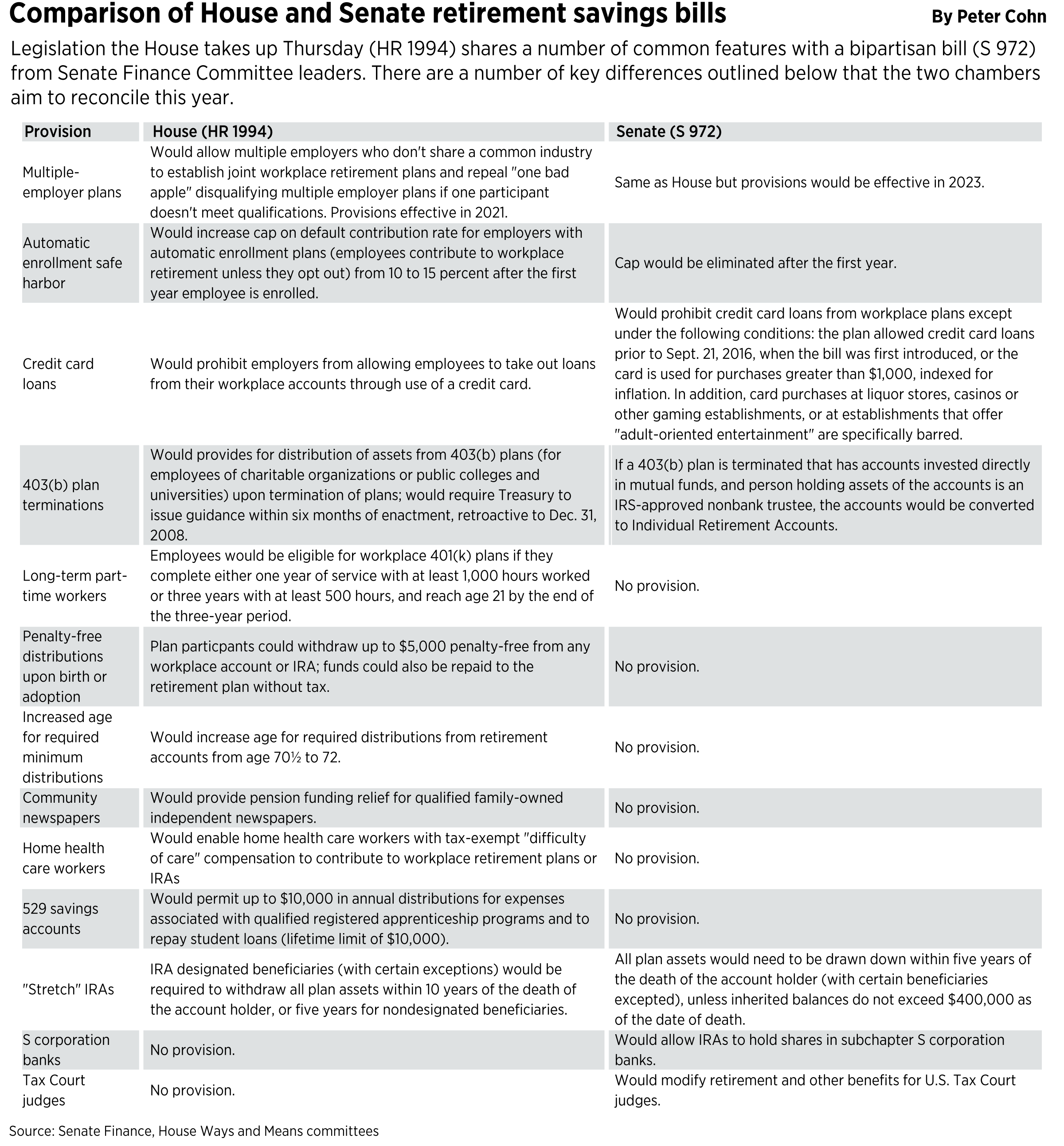

A key feature of Neal’s bill would allow companies to band together to form joint retirement plans even if they don’t share a common industry. Also among the more than two dozen provisions is a pair of tax credits, one to cut the costs for a company starting a plan and the other to encourage the creation of automatic enrollment plans, which have higher participation rates than opt-in plans.

Another provision recognizes that Americans are working longer by increasing the age for required minimum distributions from tax-favored savings plans such as 401(k)s and IRAs from 70 ½ to 72 years of age. That provision, which would cost nearly $9 billion over a decade, is the largest single benefit in the $16 billion package.

The bill is paid for mainly by requiring wealthy inheritors of IRAs to withdraw all plan assets, which would be taxable, within 10 years.

“This bill really modernizes and reforms further the private sector pension system,” said Paul Richman, chief government and political affairs officer at the Insured Retirement Institute, which represents institutional asset managers.

Adding to the bipartisan momentum is the fact that Senate Finance Chairman Charles E. Grassley and ranking member Ron Wyden are operating on much the same track, having introduced similar legislation earlier this year.

“I’m hoping that the House will send its version … over to us at some point this month,” Grassley said at a May 14 hearing. “I’ll continue to work closely with Sen. Wyden and other committee members to reconcile the differences and get this important bill to the president.”

The American Council of Life Insurers estimates the House bill’s provisions encouraging companies to band together to offer joint plans will result in about 650,000 workers gaining access to savings accounts.

Industry groups are also supporting follow-on legislation Neal is expected to introduce to require companies with more than 10 employees to offer automatic-enrollment retirement plans. That measure would provide savings plans to at least 22 million workers previously lacking access, according to the ACLI.

Neal has said his automatic enrollment bill, which he’s introduced previously, will be in the next crop of retirement legislation he pushes.

“[Grassley] indicated to me that after this passes the Senate that we will move on to a second round of increasing the opportunity for retirement savings,” Neal told the House Rules Committee on Monday.

[jwp-video n=”1″]

529 fight

While the Grassley-Wyden measure is similar to Neal’s bill, there are some notable differences.

Grassley’s bill for example doesn’t contain an expansion of uses for 529 education savings plans — a provision that briefly delayed House consideration as Democratic leaders attempted to tamp down a mini-rebellion.

Neal said a “substantial” portion of the Democratic Caucus opposed a provision to allow tax-free dollars from 529 accounts to be used to pay for home schooling and certain K-12 expenses, including at private and religious schools.

House Ways and Means ranking member Kevin Brady as well as GOP members of the Rules Committee complained that Democrats’ unilateral removal of the 529 provisions could derail future bipartisan efforts on the tax-writing panel.

Neal’s initial bill was a bipartisan effort, Rules ranking member Tom Cole said during committee debate on the rule.

“It was so good, I even co-sponsored that bill,” the Oklahoma Republican said. “This type of partisan gamesmanship is deeply disappointing.”

Neal defended the move as necessary to get the legislation through his caucus, but said it would not derail his plans for more retirement savings legislation in the 116th Congress.

“I will not let the one issue get in the way of the many big things that we have yet to do and intend to do in the next 18 months,” the Massachusetts Democrat said.

Pooled employer plans

The marquee benefit in both the House and Senate bills, estimated to lead to 650,000 more workers being covered in the workplace, comes from a collection of provisions that would remove barriers for companies to band together to offer retirement benefits.

The multiple employer plan provisions would cost $3.4 billion over 10 years, according to the Joint Committee on Taxation, as more firms set up workplace plans for which owners can deduct contributions and employees can defer tax on their contributions until retirement.

Another feature would add a new path for part-time workers to be included in their company’s retirement savings plans. Currently, people who work at least 1,000 hours a year must be included in a workplace plan, but Neal’s bill would add those who work for at least 500 hours in three consecutive years.

And a provision that benefits groups say will preserve future benefits for more than 400,000 workers in traditional defined benefit pension plans each year would modify what are known as nondiscrimination rules, which require higher- and lower-paid employees to be treated similarly in a plan. The change would allow generally older, longer-service employees to continue to accrue benefits in a plan that had closed.

Some features of the bill are appealing to conservatives, said Adam Michel, a senior policy analyst at Heritage Foundation.

Michel applauds a provision allowing penalty-free withdrawals from retirement plans in case of birth or adoption. Increasing the age for mandatory minimum withdrawals is a step in the right direction too, he said.

But Michel described as “marginal reforms” the changes that aim to encourage businesses to offer plans. “Small employers don’t get their 401(k)s in order because of the large regulatory costs that’s involved in setting them up,” he said.